Assistance is key to people’s everyday demands, health, business, or home purchases, which speeds up processes. Financial aid is a key part of making things easier. In India, different types of loans are offered to fit different types of needs. Over the years applying for a loan through different digital services has become easier. However, the variety of services offered can still create a confusion. In the next section, we will review how to go through a loan application in a simple and fast way and get information on the services offered.

1. Understanding the loan Application Process

The days of loans and lengthy paperwork filled with tedious processes are a far cry. Today loan applications are more filed with convenience in mind and can be completed quickly. Digital banking platforms made this possible and we will go through few key steps to make sure you digital banking platform is the right fit for your needs.

These are the steps to getting a loan in India.

Step 1: Identifying the loan required

Every financial requirement is different and identifying the loan is the first step. Loans are classified into various categories such as personal loans, home loans, business loans, car loans, and education loans. Identifying the purpose of the loan is the first step in getting a loan in India.

Step 2: Determining eligibility

This step is most important. Eligibility determines whether you get a loan or not. Different loans require different eligibility. For instance, personal loans require a fixed minimum monthly salary, while home loans require you to have a stable job and a good credit score ranging to a certain figure. Eligibility checking can be done using the lender’s website or an eligibility calculator.

Step 3: Pricing the loans

This is a very important step. Pricing can include a variety of different things like interest rates, repayment terms, and processing fees. If you do not compare the loans, you can get a bad deal. Comparing loans can be done on various platforms online.

Step 4:

Once you’ve chosen a lender and loan type, the next thing to do is fill out a loan application. Most banks and financial institutions now have online portals, which is great for people who like the ease of digital options.

Step 5:

After the application form is filled out, certain documents must be submitted for verification. In this case, the documents usually consist of your identity proof, address proof, income proof, and other financial documents. Most lenders let you submit documents digitally, which speeds up the process a lot.

Step 6: Getting Your Loan Approved and Sent to Your Bank

Before your loan gets approved and the money gets sent to your bank, the lender must first receive the application and accompanying documents, and may approve or deny your loan request. if the loan is approved from your lender, the loan amount is either sent to your bank, or directly sent to the provider if your loan is for home and education-related expenses.

Section 2: Loans in India

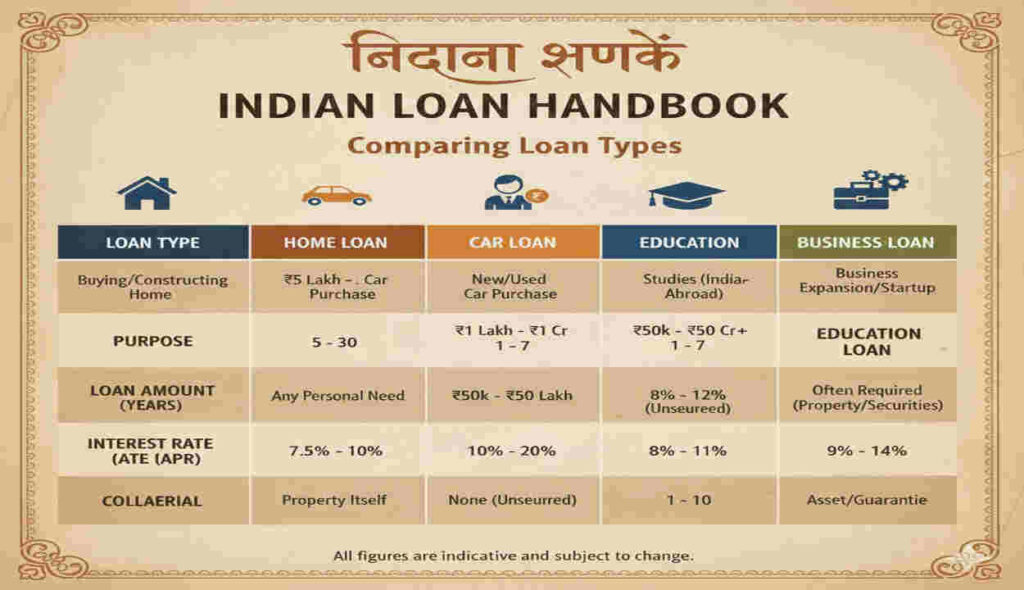

Loans in India also have their own special set of purposes. know the following to be able to help identify the right one: Use the table below as one of the most common loan types to know the most of the types of loan in India:

| Type of Loan | Purpose | Interest Rate Range | Loan Amount | Repayment Term | Eligibility |

| Personal Loan | Personal emergencies or needs | 10% – 24% | ₹10,000 – ₹50 Lakhs | 1 – 5 years | Minimum monthly income, Good credit score |

| Home Loan | Purchase or construction of a home | 6.5% – 8% | ₹1 Lakh – ₹2 Crores | 10 – 30 years | Stable income, Good credit history |

| Business Loan | For business expansion or startup | 12% – 22% | ₹50,000 – ₹5 Crores | 1 – 5 years | Established business, Financial documents |

| Car Loan | Purchase of a car | 7% – 15% | ₹1 Lakh – ₹50 Lakhs | 1 – 7 years | Stable income, Car type eligibility |

| Education Loan | Higher education | 7% – 12% | ₹50,000 – ₹1 Crore | 5 – 15 years | Stable income, Car type eligibility |

3. Factors to consider before getting a loan

Now that the loan application process is straightforward, there are certain factors that you should think through one last time before getting a loan. They are as follows:

Interest Rate

The interest rate is the key factor in determining how much the loan in total will cost you.

Interest rate difference may seem small, but compounding works wonders over years. You must compare lenders.

Processing Fees

Fees associated with loan application processing (the processing fee) are a one-time charge that most lenders are required to collect. They are typically 1% to 3% of the loan. Be sure to include this in the total cost of your loan.

Prepayment and Foreclosure Charges

If you plan on paying the loan off before the end of the term, some lenders have a charge for that. Be sure to look out for this if you are going to pay off your loan early. These are called prepayment or foreclosure penalties.

Loan Tenure

Having the right tenure is the most important thing to consider when trying to control how much you pay in EMIs. With a longer tenure, you pay less in EMIs, but end up paying more total interest and with a shorter tenure it gets a bit more complicated in that you are going to pay more in EMIs, but you are also going to pay less total interest because you are paying it off in a shorter time.

Requirement to Apply

Every loan has individual requirements, so make sure to review them to make sure you are not wasting anyone’s time.

4. Ways to Make Applying for a Loan Easier

- Look at Your Credit Score: Credit score increases the chances of getting a loan so make sure to check yours beforehand.

- Do not apply for a lot of loans at once: This lowers your chances of getting a loan and hurts your credit score. do your research and apply for the loans you are most eligible for.

- Parts With Your Documents Carefully: Make sure to give the lender the right documents. If you mess up or forget a part of the documents the lender may take a long time processing your document or may reject your document.

- Look at the Rules: Before you get the loan take time to make sure you understand the rules and guidelines. Especially the small rules to avoid problems later on.

5. Conclusion

The best part about applying for a loan in India is how easy it is. Thanks to online loans and digital banking getting a loan is easier than ever. Loans are different and so are the payments and eligibility requirements. However, in order to not have any issues getting a loan, it is important to measure, compare, and pick the right loan for your requirements. You have a loan hassle in your search, so narrow it down most effectively. It can help ease the burden of financial worries, and it is a pivotal part of your loan search.

Do you want to start a hobby? Buy a house? Grow a business? You can use these loans for all of that. Simply learn more about the loans to make better financial choices.

Using this guide, you can learn everything you need to know about getting loans in India. It provides a complete overview and thorough comparison of all loans that are available to you. It can explain to you what loans are best for your financial situation. It can help you achieve your goals and make your financial situation far better and help you achieve most of your goals.